In 2017 a group of central banks and financial supervisors formed the Network for Greening the Financial System (NGFS), to work out how to future-proof the global financial system from climate change. Now its 83 members – including its newest and most powerful, the US Federal Reserve – are leading efforts to stress-test the climate resilience of countries’ banks.

There is a lot of overlap between the NGFS and the G20 Financial Stability Board (FSB), both in terms of membership and agenda. The FSB set up the Taskforce on Climate-related Financial Disclosure (TCFD), whose framework for disclosure is transforming corporate climate-related reporting. However, while the TCFD focuses on improving private sector disclosure, the NGFS is trying to build capacity among regulators to understand what climate-related information they need from their supervised entities, and what to do with it.

The NGFS achieved a milestone in June last year with the release of a first set of climate scenarios to guide climate risk analysis by financial institutions. These scenarios set expectations not just among financial regulators around the world but across financial institutions more broadly – and thence to the companies they invest in.

What can the NGFS scenarios tell us?

The NGFS scenarios draw from a broader set of scenarios that underpin climate change research by the Intergovernmental Panel on Climate Change (IPCC). The NGFS’s selected scenarios indicate some interesting priorities:

- The initial focus is on transition risk. These are the risks associated with efforts to reduce greenhouse gas emissions. NGFS scenarios are categorised as follows:

- “Orderly” (broadly consistent with the goals of the Paris Agreement)

- “Disorderly” (delayed or constrained action requiring sharper emissions reductions to meet the same target)

- “Hot house world” (continued inadequate decarbonisation that results in 3°C+ of warming).

- “Disorderly transition” is a major concern. The phrase is a bit of an understatement, but “disorderly transition” refers to emissions reduction efforts that are disruptive and unplanned, resulting in economic shocks, technology constraints and stranded assets. The NGFS has identified two factors that drive disorderly transition:

- Delayed action: policies remain on track for 3oC warming until 2030, at which point countries adjust policy settings to rapidly decarbonise in line with the goal of limiting warming to well below 2oC or 1.5o The need for dramatically deeper emissions reductions after 2030 drives higher carbon costs and curtails the use of so-called bridging technologies such as natural gas

- Limited carbon dioxide removal: this tests the assumption built into many models that the world can offset emissions with high volumes of carbon sequestration or even negative emissions later this century. Restrictions on the total amount of available carbon dioxide removal results in the need for earlier and deeper emissions reduction.

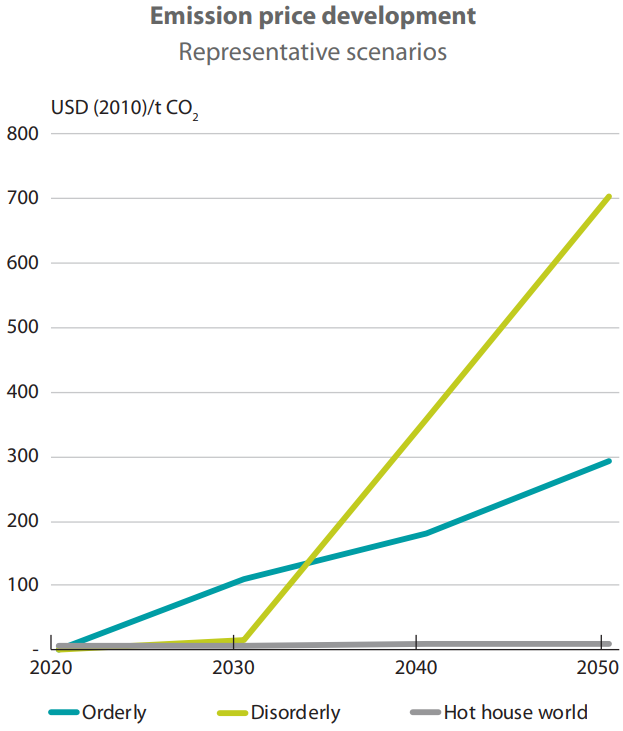

The NGFS’s core disorderly transition scenario incorporates both factors. This scenario’s carbon price, compared with that of the core orderly transition scenario in Figure 1 below, reflects the significant additional costs associated with these two forms of disorderliness. However, since the scenario assumes eventual achievement of the desired temperature goal, it does not account for the greater risk of failure in a disorderly transition.

Figure 1: Carbon pricing in NGFS core scenarios [1]

Given that disorderly transition presents significantly greater transition risks – and that, more arguably, the path to 1.5oC or 2oC is more likely to be disorderly than orderly – organisations need to start investigating disorderly transition scenarios. They have been explored by some organisations – for example BHP’s “shock event” decarbonisation scenario, or the PRI’s Inevitable Policy Response – but have not been in widespread use, possibly because of their additional complexity. This will probably change, now that the NGFS has provided a template, and members such as the Bank of England have explicitly required analysis of disorderly transition.

What can’t they tell us?

- The NGFS scenarios provide global and some regional results – but no outputs specific to Australia. This may be less of a problem for elements like technology cost projections, especially given the uncertainty around projected technology costs anyway, but it is a big problem for physical risk. Having said that, a broader problem with the models underpinning the scenarios is that their assumptions are highly conservative and not easily accessible. Because of these features, the NGFS scenarios are best considered as broad-brush indications of the scale of potential transition impacts only.

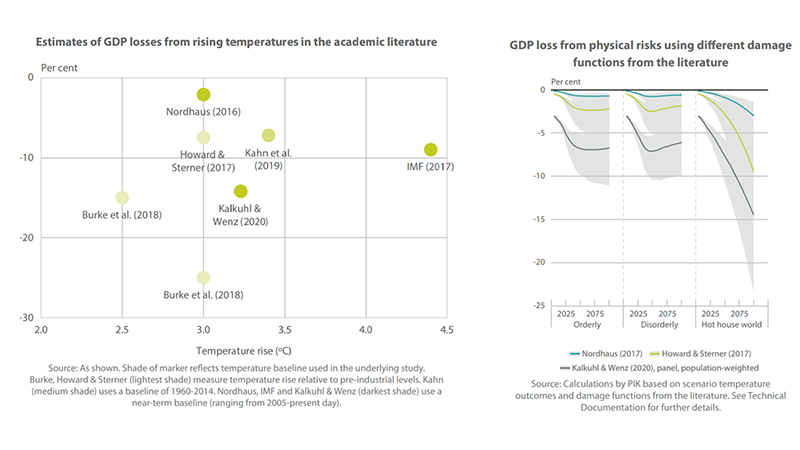

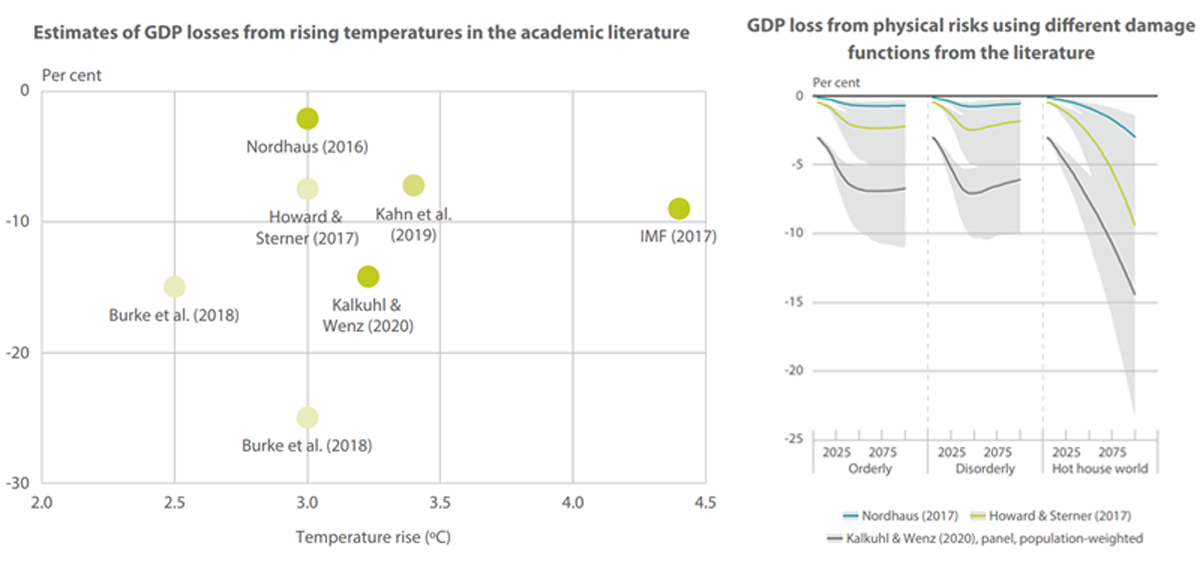

- Data on the costs of physical climate change are rudimentary. A characteristic of the IPCC scenarios is that economic damages from physical climate change are not incorporated into transition scenarios. As an initial workaround, the NGFS provides estimates of GDP impacts that have been calculated separately based on three damage functions and are provided at a global scale only. The NGFS notes that these are likely to underestimate the costs of climate change.

Figure 2: Estimates of climate change’s impacts on GDP from research literature (left) and used in NGFS scenarios (right), extracts from NGFS (2020) [2]

- Physical climate data is limited and of little value to Australia. The NGFS scenarios include some chronic climate change impacts including changes in temperature, precipitation and agricultural yields. However, aside from the fact that many other physical variables need to be considered to analyse the impacts of physical climate change on an economy, the scale at which the included variables is provided makes them unusable in Australia. Physical risks are locationally specific and require downscaled analysis at the asset level. Global scenarios do not provide sufficient granularity to accurately project physical impacts at the subnational level, requiring more detailed modelling for each market.

The NGFS has acknowledged these weaknesses and launched a research program to address them. A planned release of updated, more sophisticated scenarios has been delayed due to the coronavirus pandemic.

What does this add up to?

The broad contours of the scenarios will shape financial stress testing globally, and present a valuable framework for non-financial companies to undertake scenario analysis as well. However, the devil is in the lack of detail: the lack of regionally specific inputs and outputs means that Australian companies will need to look elsewhere for relevant and reliable data sources. It is important to remember that Australia’s economy is unique not just in its combination of emissions-intensive activities and physical climate exposures, but in the role played by its land sector. Models that fail to capture Australia’s circumstances cannot be trusted and do not provide a reliable view of Australia’s sovereign risk. Central regulators need to ensure financial stress testing caters for Australia’s unique characteristics.

A paper in science journal, Nature Climate Change recently considered the risks of inappropriate uses of climate-related data. The paper noted that decision-makers and preparers of financial reports may misplace trust in climate information, leading to, on one hand, a false sense of security regarding an entity’s climate position or, on the other, the withdrawal of capital from areas assessed as ‘risky’ that under alternative modelling specifications would be considered ‘safe’.

In light of these concerns, the NGFS scenario resources should be treated somewhat cautiously – less as robust guidance to climate-related risk analysis, rather as a useful starting point for more granular investigation.

References

[1] NGFS | NGFS Climate Scenarios for central banks and supervisors (June 2020)

[2] NGFS | NGFS Climate Scenarios for central banks and supervisors (June 2020)

Related insights

Get our thought leadership directly to your inbox

Keep up to date with the latest insights on net zero, climate resilience and clean energy transition.