Part two of Anita Stadler's two part series on Large-scale Generation Certificates (LGCs)

Energetics has been working extensively over the last 18 months with large energy users exploring a range of options to deal with the current market challenges associated with high LGC prices and policy uncertainty surrounding the renewable energy target. Options vary, depending on the strategy and risk appetite of energy users. Nonetheless, for large energy users there are a number of proactive strategies that can assist your business to manage the risks.

What are the risks of not being proactive?

Unless large corporate energy users are proactive, they will have to brace themselves to be on the receiving end of LGC prices close to the penalty rate over the next four years, and possibly longer.

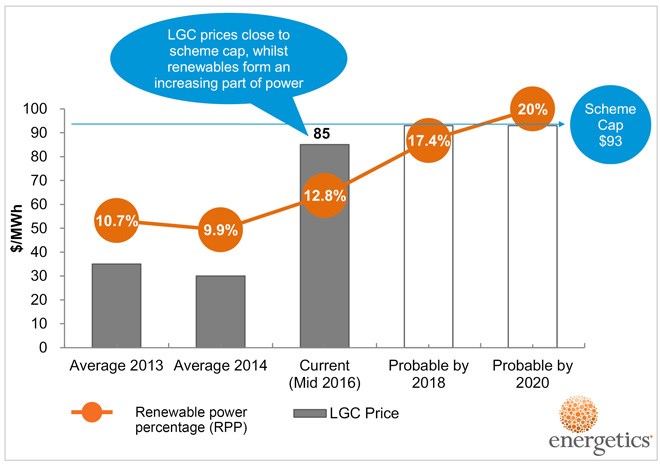

For many who concluded electricity contracts with a fixed LGC pass-through cost in 2013 or 2014 when LGC prices were around $35, a jump to the current level of around $85/MWh will drive up their LGC pass-through cost by 143%.

This is equivalent to ~10% of the negotiable portion of the electricity bill, or more than $500,000 per annum for a user consuming 100GWh per annum. This will increase to ~15% as the renewable power percentage (RPP) under the RET steps up to 20% by 2020, from the current level of 12.75%.

Figure 1: RPP and LCG price correlations

Energy users coming out of long term electricity contracts for grid supplied power and / or without their own significant own decentralised power generation capacity, will need to prepare themselves for higher and more volatile electricity prices and environmental charges.

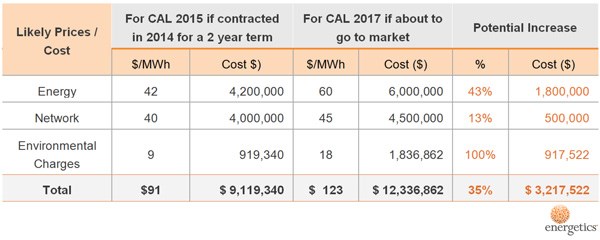

It is essential to review existing budget assumptions for energy. As illustrated below for a corporate consuming 100 GWh per annum and about to reapproach the market for two year contract, the electricity budget provision for 2017 may need to increase by as much as 35% compared to 2015.

Table 1: Electricity budget provision comparison

Options for business to manage the risks

Below are some strategies that can be pursued.

- On-site generation opportunities. The high price of LGCs challenges the previously held view of sizing on-site solar projects <100kW to maximise upfront Small Scale Technology Certificate (STC) benefits. While this is still a good option is many cases, consideration should also be given to up-scaling solar systems to self-generate LGCs, which are trading at more than double the price of STCs. Alternatively, suppliers may be willing to enter into PPAs where they offer a lower rate, whilst taking the long term LGC price risk

- ‘Self-source’ LGCs to offset obligations under the RET scheme (currently passed through by the retailer). This would typically require a five to ten years commitment and can be undertaken by corporate entities, but a buying group may be more attractive for organisations with limited LGC requirements and in-house capacity to manage the transaction.

- Entering into a 10 year or longer renewable energy offtake agreement for the supply of power and LGCs (i.e. bundled). Energy users have the option to use LGCs additional to the Renewable Power Percentage (RPP) to meet their own emissions reduction targets or trade surplus LGCs over the counter to reduce their energy costs. Various contracting and pricing models can provide different levels of certainty for both power and LGCs. The option most suited to an organisation is best explored on a case by case basis.

Irrespective of whether businesses adopt any of the above strategies, or persist with conventional procurements strategies, it is essential to review existing energy budget assumptions for electricity as well as environmental charges.

The benefits of taking control of your LGC and / or power supply

The combined power of a large number of end users that take the above proactive steps could facilitate a shift in the renewable energy market, currently characterised by asymmetric competition. This trend is well under way in global markets where more than 50 large multi-nationals ranging from Google, 3M, P&G, DuPont, Nestle, Unilever and Walmart have signed up to Corporate Renewable Energy Buyer’s Principles and are actively pursuing strategies to add renewable energy to their own facilities or are entering into contracts to buy or invest in off-site facilities.

Australia, with the exception of a handful of Government and private sector organisations, is lagging behind international peers. Taking control of your LGC or power supply in a market has obvious benefits, as outlined below.

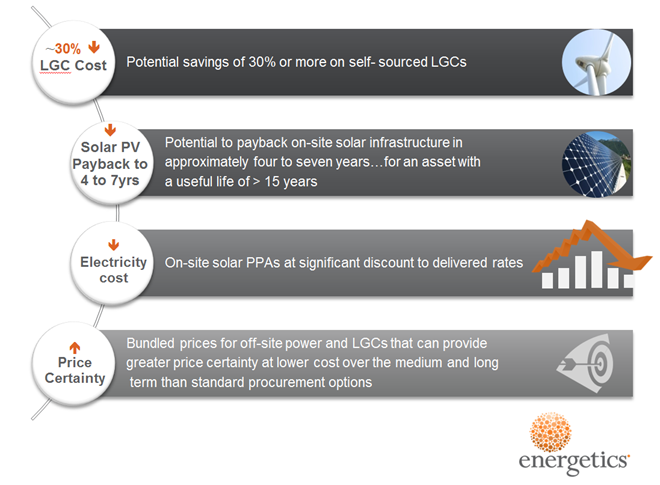

Figure 2: LCG and power supply market benefits

However, pursuing these strategies in the Australian market carries some unique risks. It is essential to partner with experienced providers and consultants that understand the technological, financial, legal, energy market and policy challenges and opportunities to guide your executive team to make informed decisions.

Energetics has more than 30 years’ experience advising large energy users from across all sectors of the Australian economy. Specifically, we have worked on the ACT Government's reverse auctions, the implementation of on-site renewable energy strategies for a large Federal Government Agency and numerous corporate clients, as well as supporting the Sydney Metro North West renewable energy procurement process and the Melbourne Renewable Energy Purchasing Group. We follow developments in the National Electricity Market and Western Australian Electricity Market on a daily basis, and have an in depth understanding of the federal and state regulatory environments that are shaping the energy mix.

For further insights and to help your business assess and manage its risks, please contact any one of our experts.